Savings Planner That Actually Works in 2026

Hey everyone, it's Ren here. For years I tried to save whatever was left at the end of the month.

You can guess how that went. There was never anything left. It was like trying to fill a water bottle by cupping my hands under a running tap, most of it just ran straight through my fingers. The fix was almost embarrassingly simple: put the bottle under the tap first.

That is what a savings planner does. It puts the bottle first. The saving happens before the spending gets a chance to run through your fingers.

"Do not save what is left after spending, but spend what is left after saving." — Warren Buffett

🔍 Why "save what's left" never works

Saving whatever remains sounds sensible, but it quietly fails for a few predictable reasons, and none of them mean you are bad with money:

- Spending expands to fill whatever is available, so "what's left" trends towards zero.

- With no target, there is nothing to aim at and nothing to feel good about hitting.

- Without a date attached, a savings goal stays a vague someday rather than a real plan.

- You cannot see progress, so there is no reward loop to keep you going.

A savings planner fixes all of that by flipping the order and adding a finish line.

✅ How a savings planner works

- Name each goal. Emergency fund, holiday, house deposit, new car. Vague "save more" becomes specific.

- Attach an amount and a date. $6,000 by next December. Now it is a target, not a wish.

- Let the planner do the division. It works out the monthly contribution each goal needs. $6,000 over twelve months is $500 a month, plainly. You can run the same sum in seconds with our free savings goal calculator.

- Treat that contribution like a bill. It comes out first, not last. Automate it the day after payday if you can.

- Watch the bar fill. A visible progress bar is what turns saving from a chore into something quietly addictive.

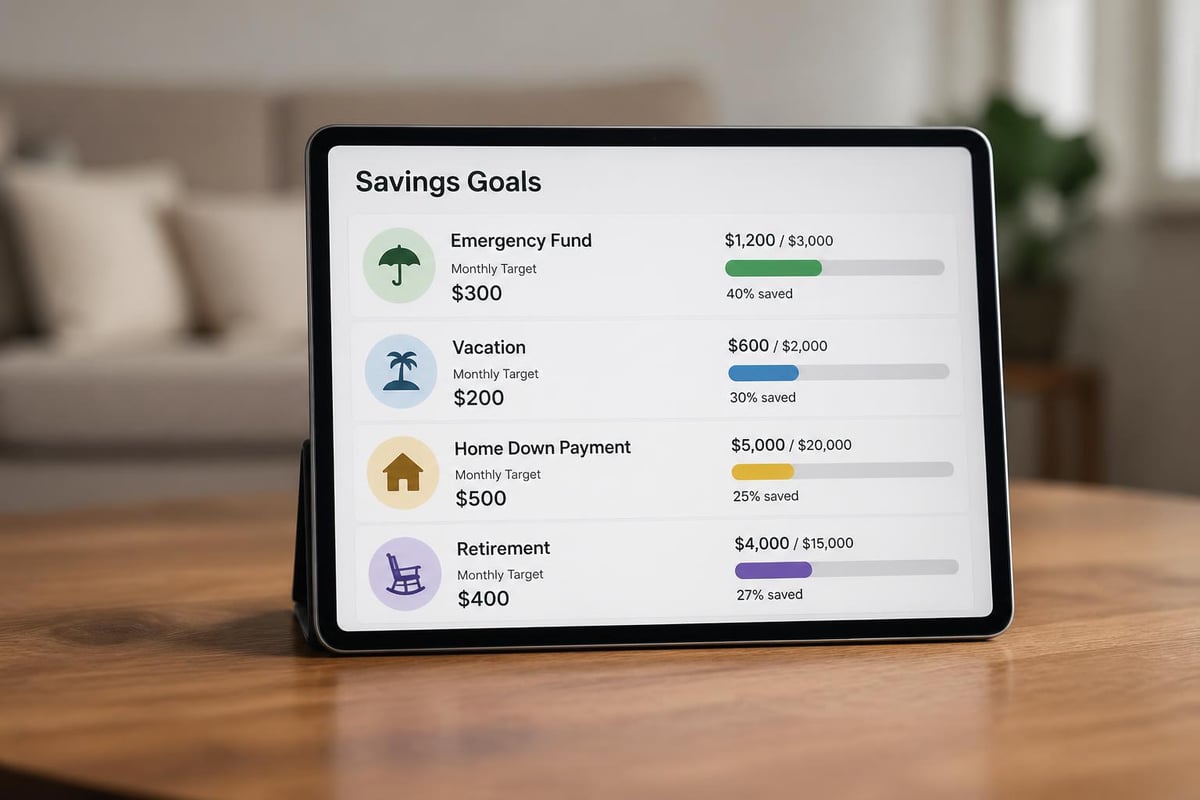

Juggling more than one goal

Most of us are saving for several things at once, and that is fine. A good planner lets each goal have its own line, its own amount, its own date, and its own progress bar. If the total monthly contribution is more than you can manage, the planner makes the trade-off visible, so you can consciously stretch a date rather than quietly abandon a goal.

🚫 Savings planner mistakes to sidestep

- Saving last instead of first. Fix it: move the money the day after payday, before spending can claim it.

- Goals with no date. Fix it: every goal gets a deadline, or it stays a someday.

- One vague "savings" pot. Fix it: separate goals, separate lines. Mixed-up savings are easy to raid.

- Setting a contribution you cannot sustain. Fix it: plan with a number that survives a tight month. A smaller amount you actually keep beats a big one you abandon.

Want the planner already built?

You can build your own, and the steps above are the whole method. But if you would rather skip the setup, the Ultimate Budget System has multi-goal savings tracking with contributions, dates and progress bars built in, alongside your full budget. Set it up once and it runs the year. Trusted by over 70,000 customers.

Get the Ultimate Budget System →🎯 Your action steps this week

- Write down every savings goal you have, however small.

- Give each one a target amount and a real date.

- Work out the monthly contribution each needs (amount divided by months), or let our free savings goal calculator do the maths in seconds.

- Set up an automatic transfer for the day after payday.

- Pop a progress bar on each goal. To free up the money to fund them, pair this with our zero-based budget template guide.

A savings planner does not require more willpower. It just changes the order, so the bottle goes under the tap first, and the saving actually happens instead of running through your fingers.

❓ Frequently asked questions

What is a savings planner?

It is a tool that turns savings goals into specific monthly contributions and dates, then tracks your progress, so "save more" becomes "$500 a month, debt-free of this goal by December."

Should I save or pay off debt first?

Most people do best building a small emergency buffer first, then balancing extra debt payments with longer-term saving. A planner lets you see both moving at once.

Can I track more than one savings goal?

Yes, and you should. Give each goal its own line, amount, date and progress bar so they do not blur into one easily-raided pot.

How much should I save each month?

Whatever you can sustain on a normal, slightly tight month. A consistent smaller amount beats an ambitious one you abandon after two months.

You have got this. Bottle under the tap first, one filled goal at a time.

To your financial freedom,

Ren

About Ren

Ren is the founder of JRen Digital, home to minimalist budgeting and debt spreadsheets trusted by over 70,000 customers worldwide. Ren writes practical, no-nonsense guides that help everyday people take the stress out of money. Explore the full range of templates at jrendigital.com.

Keep reading

- Savings Goal Tracker Spreadsheet That Holds Every Jar

- Emergency Fund Spreadsheet That Fits Your Real Month

- Sinking Fund Tracker Spreadsheet That Beats the Slip

- Saving Tracker Template: Simple Tools for Financial Goals

- Budget Template That Actually Works in 2026

- Budget Spreadsheet: The One You Actually Keep Using (2026)

- Budget System That Actually Works in 2026

This article is for general information only and is not financial advice. It does not take into account your personal situation, needs or objectives. Please consider speaking with a qualified financial adviser before making financial decisions.